NVIDIA completed a $25 billion high-grade bond offering — its first since 2021 — to fund the AI buildout, after order books swelled past $85 billion and pushed the deal up from a $20 billion target. Shares slipped about 1.7% on June 16 to around $208.86, with the company holding a roughly $5.1 trillion market cap. The pullback came despite blockbuster demand for the debt.

Micron jumped about 11% Monday to a record near $1,089, up more than 700% on the year, as Wall Street piled on price-target hikes. Cantor Fitzgerald more than doubled its target to $1,500, with TD Cowen, RBC and Aletheia at $1,500, $1,200 and $1,600 — and some calls reaching $1,750. HBM memory is sold out through all of 2026, with earnings due June 24.

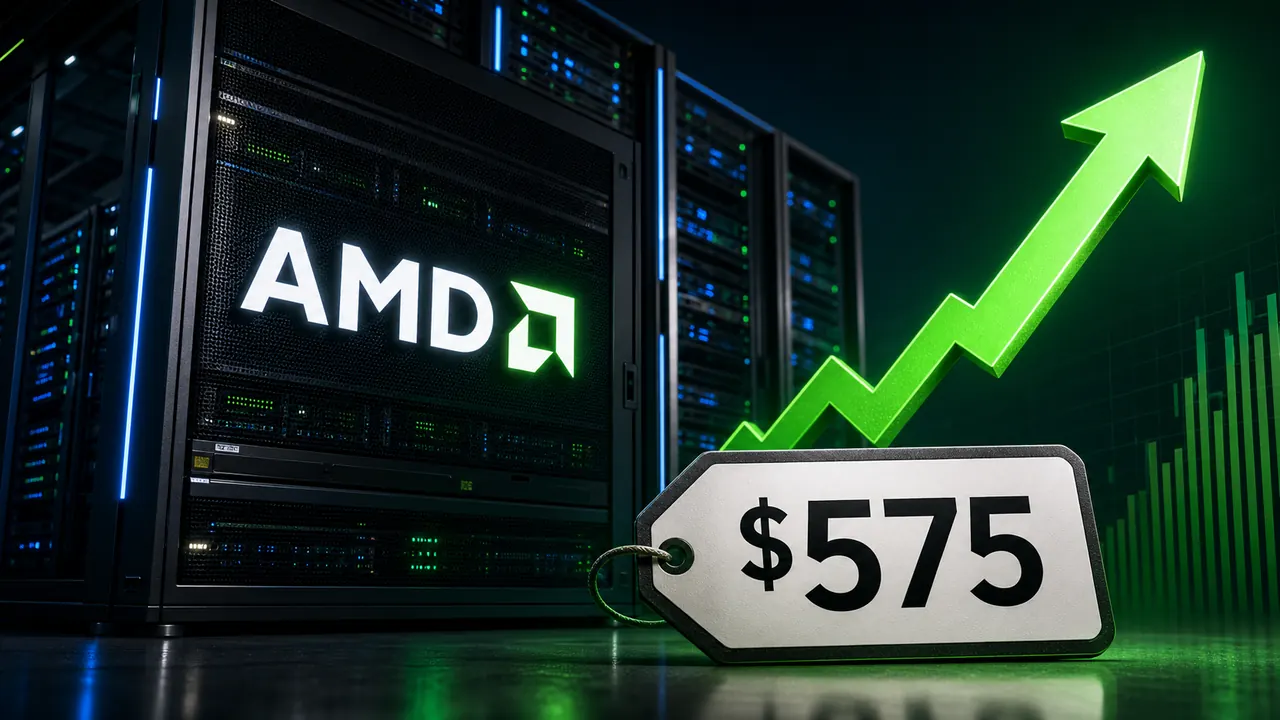

AMD climbed about 6.98% Monday to roughly $547 after Citigroup upgraded shares to Buy from Neutral and raised its target to $575 from $460, citing AMD's growing role as a credible second source of AI silicon. The analyst flagged Meta as an undiscounted buyer of MI-series GPUs. The MI400 series, projected at $7.2 billion in first-year revenue, anchors the bull case.

Arm Holdings led the chip complex Monday with an 8.33% gain to about $412.55, extending a roughly 97% one-month run. Wells Fargo lifted its target to $410 and Mizuho went to $500, both citing demand for dense, efficient CPUs to run agentic AI workloads in hyperscale data centers. Arm's record fiscal Q4 saw revenue up 20% to $1.49 billion, with data-center royalties more than doubling.

The Philadelphia Semiconductor Index surged 5.4% Monday after a U.S.-Iran peace deal reopened the Strait of Hormuz, easing energy fears and sending the Nasdaq up 3.1% and the S&P 500 to a record 7,554. Falling Treasury yields gave long-duration AI and software names an extra tailwind. Lam Research added 6% on an Oppenheimer target hike to $400.

Anthropic has confidentially filed draft IPO paperwork, potentially beating rival OpenAI to Wall Street as soon as this fall. The move follows a $65 billion Series H that valued the company at $965 billion — surpassing OpenAI's $852 billion mark — on a reported $47 billion revenue run rate. Anthropic and OpenAI remain private, so this is a funding and IPO watch item, not a tradable name.

Palantir rose 5.25% Monday to $134.71 as Treasury yields fell on the Strait of Hormuz peace news, a tailwind for long-duration software valuations. The stock remains down about 24% year-to-date despite a roughly 101% three-year gain. Palantir's Q1 results showed strong U.S. revenue growth and a raised full-year outlook.

Broadcom traded near $394.82 on June 16, with bullish analyst coverage on its custom AI silicon franchise. The company counts Anthropic, Google, Meta and OpenAI among six core ASIC customers and reiterated AI semiconductor revenue guidance above $100 billion, with momentum carrying into fiscal 2027. Notably, Broadcom signaled it will sell chips-only rather than full integrated AI systems.

Oracle reported record fiscal Q4 and FY26 results, with Q4 revenue of $19.2 billion (up 21%) and cloud infrastructure revenue of $5.8 billion, up 93%. Full-year cloud revenue hit $34.0 billion, up 39%, while remaining performance obligations have ballooned to hundreds of billions. The open question is whether a roughly $50 billion fiscal-2026 capex commitment pressures margins.

SoundHound AI rose about 8.48% to close near $7.49 after being named overall Leader in ISG's 2026 Buyers Guide for Conversational AI emerging providers. The report spotlighted SoundHound's new OASYS agentic platform as a self-learning system for orchestrating conversational agents across channels. It's a smaller name, but a reminder that voice AI is drawing real enterprise validation.